Think it’s too late for tax optimization strategies in your business? Or that tax optimization only works for companies flush with cash? If you think either of these, think again.

Tax optimization strategies are familiar to large businesses and corporations because they understand the potential cash savings and are comfortable investing time and resources upfront for significant long-term savings. Although tax planning and optimization strategies are a part of many prominent business strategies, the average small business owner or early-stage founder may prefer to avoid thinking about taxes.

After all, tax planning isn’t bringing in revenue for your business; it’s activity and operations. Even though tax optimization strategies may not drive sales, they can help you keep more of the money you make in your pocket.

This post explores effective tax management strategies to implement before the end of the year.

Review Your Current Tax Situation

The ever-changing tax code can significantly impact your business, so staying up-to-date on what’s new and what might be coming is essential. The best way to start is by reviewing your business’s current tax situation and analyzing its current standing.

Small business owners need to stay informed about how changing tax laws will affect their operations so they can adapt accordingly and avoid negative impacts on the bottom line.

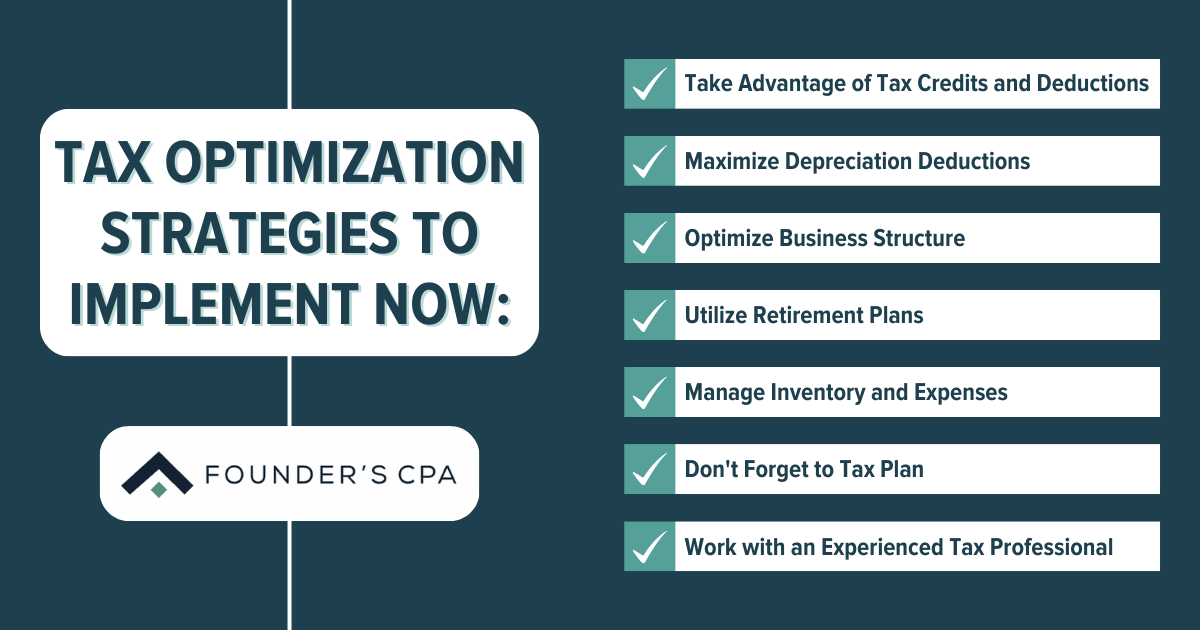

Tax Optimization Strategies for Businesses

Fortunately, with the help of a knowledgeable accountant, you can define strategies to ensure you’re not paying more taxes than necessary.

Take Advantage of Tax Credits and Deductions

Many tout tax credits as the best way to reduce taxes, but deductions can be just as valuable. A tax credit reduces your tax obligation dollar-for-dollar, whereas a deduction reduces your taxable income. Both can have a positive impact on your bottom line.

For example, suppose you invest in equipment that reduces your company’s energy usage and saves money on utilities. You may be able to deduct the equipment cost from your taxable income (but may need to depreciate it over several years). Plus, your state, local, and federal governments may offer additional credits or incentives for improving energy efficiency.

Both situations could mean a lower tax bill.

Maximize Depreciation Deductions

Depreciation is a tax benefit that allows you to spread a portion of the cost of your business assets throughout their useful life.

Imagine buying a powerful computer for your company with a three-year useful life.

By taking advantage of this deduction, you can:

- Spread the cost over three years

- Reduce your taxable income

- Save money on taxes

The amount of depreciation you can claim depends on the type of asset you purchase and how you use it.

Optimize Business Structure

Certain types of entity structures can be more efficient in certain situations, and you can change the structure of your business to make it more tax efficient.

For example, if you have an S-corporation but want to be taxed like a C-corporation, you could convert your S-corp into a C-corp. This change allows you to take advantage of certain tax breaks for small businesses that aren’t available to S corporations.

Utilize Retirement Plans

Investing in a retirement plan can help reduce your business and personal taxable income, lower your tax bills, and increase your long-term financial security.

Depending on your business structure, you can contribute to a 401k or 403b retirement plan to save for your and your employees’ futures while enjoying lower taxable business income. There are also IRAs available for certain types of businesses.

Manage Inventory and Expenses

Managing inventory and expenses means ensuring your business purchases are:

- Necessary

- Cost-effective

- Well-timed

If you need to purchase additional products or services, ensure they are the best possible value for your company.

The inventory cost only counts as expenses once the inventory is sold, so be mindful of how much inventory you hold at any given time. Some states even treat inventory as property and tax it.

Don’t Forget to Tax Plan

While tax planning isn’t something most people focus on, it’s essential for any small business owner who wants to succeed in today’s economy. You must pay attention to taxes from the beginning of your business because even minor mistakes can significantly impact your bottom line.

For example, you could be penalized for setting up your books incorrectly, forgetting to file on time, or not paying promptly. These annoyances will cost you money and take time away from growing your business.

Work with an Experienced Tax Professional

Taxes can be the most significant single expense many businesses will ever face. Like with many topics in business and private, a little planning can go a long way to reducing stress and cost.

As many of these optimization strategies need professional implementation, it pays to consider hiring an accountant to help you decide which fits your business.

A competent tax professional can help you identify deductions and credits you may have missed and highlight gaps in your entity structure and inventory management. They help reduce your tax burden and save money while ensuring your business operates legally and intelligently and isn’t underpaying.

Your tax strategy could probably use some optimization, and Founder’s CPA can help. Contact us today to find out how.